About the client

An innovative European multinational company and world leader in the renewable energy sector specializing in generation, distribution, and trading of electricity (renewable, solar, wind, and hydro) and the distribution and trading of gas.

Challenge

Managing counterparty credit risk exposure

Volatility in energy prices and ongoing geopolitical tensions have resulted in a greater risk of counterparty credit exposure with customers and trading partners. As a result, our client was seeking to enhance their early warning system and credit risk quantification methods.

Solution

Innovative credit risk solution that offered actionable insights

With private companies reporting their fundamentals at various frequencies and sometimes with large delays, it can be difficult to accurately detect a possible deterioration in creditworthiness. Moody’s provided an innovative credit risk solution that offered actionable insights like: Probability of Default (PD) level, PD Implied Rating, PD change, peer analysis as well as early warning risk quadrants –all helping the client stay one step ahead!

Spot subtle signs of credit deterioration to make informed decisions

Using enhanced early warning alerts, the client’s credit team was able to spot subtle signs of credit deterioration before they become catastrophic problems—resulting in more informed decision making towards effective risk management. Here’s what the client did to identify such important indicators when evaluating public or private companies in their portfolio with limited or no financial information.

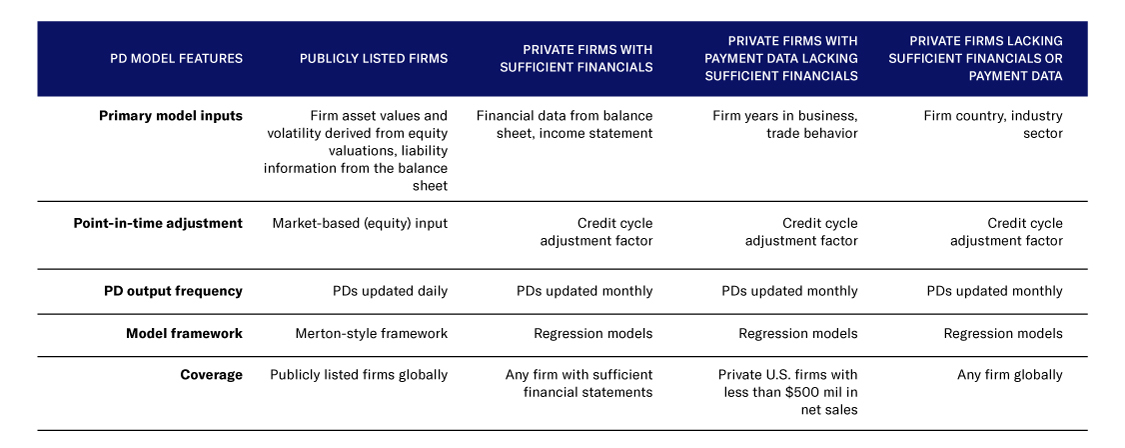

Moody’s Analytics PD models cover an entire corporate credit portfolio

Although Moody’s PD models are derived using different data inputs and different modeling methods, the models all yield forward-looking, point-in-time probabilities of default. They are updated monthly or daily and serve as a solid foundation for early warning of credit risk.

Pre-calculated, point-in-time PDs for 520+ million firms globally

Since Moody’s rating scale is well known throughout the industry, our implied rating metric unlocked value for the firm by demonstrating where investment grade quality is available for investors. In practice, that means that our Early Warning System can screen for material changes in credit risk for any firm in an automated way, without the need to input data or manually run models.

How it works?

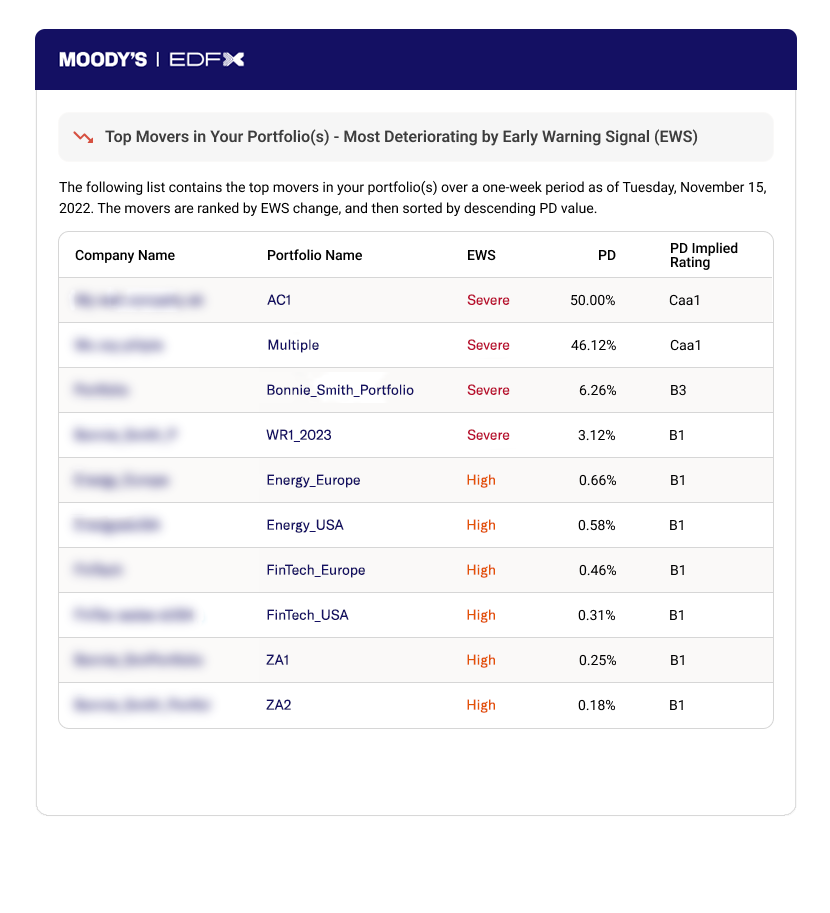

Customized alerts so no risk is left undetected

The client received regular alerts at a customized frequency for their existing portfolio companies and other company names or industries they want to track. These alerts, in a simple and concise manner, show the change in PD levels, PD Implied Ratings and risk category on our Early Warning System for the tracked companies enabling credit teams to take timely action for the identified risk/opportunity.

Key benefits to the client

An automated workflow helped the client work more efficiently

Impact

Immediate efficiency gains in credit monitoring and counterparty risk management

The client can now access an improved and efficient early warning solution taking into account credit quality momentum and relative strength. They can better manage their diverse portfolio of counterparties through accurately measuring of default risk of a combination of public and private firm models allows for a global view and coverage of almost any-size obligor.